Catching up on old taxes starts with filing, not fear. You can usually file the current year and two prior years electronically, while older years go by mail. You claim a refund for most prior years only if you file within three years of the original due date, and you risk losing credits like the Earned Income Credit if you miss that window. If you owe, the IRS adds penalties and interest each month until you set up a payment plan or pay in full. Social Security retirement benefits face a 15% federal levy when tax debts sit unpaid, so filing and arranging payments protects your benefits and credit story. File even if you cannot pay in full, because filing cuts penalties and shows good faith.

Why you should file your past due return now

Filing old returns puts you back in control. You stop failure-to-file penalties from stacking, you start the clock on collection timelines, and you position yourself for payment relief. You also protect refunds that the law may still allow you to claim. You remove the risk that the IRS files a substitute return based on limited data that overstates your tax bill. You clear the way for loans, mortgages, and professional licenses that often ask for recent filed returns.

Key benefits in plain terms

Filing shuts down one of the costliest penalties. Filing unlocks payment options and stops the fear spiral. Filing gives employers, lenders, and schools the proof they need. Filing also reduces the odds of enforced collections like levies and liens.

Avoiding IRS penalties and interest charges

For a deeper dive on relief, see our blog on IRS penalty abatement strategies for first-time abatement and reasonable cause steps.

Late filing costs more than late payment. The failure-to-file penalty runs higher than the failure-to-pay penalty, so you cut your losses when you file first, then pay what you can. Interest compounds until you resolve the balance, so an installment agreement helps control the damage. The IRS may also reduce penalties if you qualify for first-time abatement or prove reasonable cause. File now, then request relief with facts and dates.

What to do this week

File the oldest unfiled year you can finish fast. Pay something with each filing to reduce interest. Apply for a payment plan online to pause collection pressure. Keep all mailed proof and transcripts in one folder for each year.

Our services at Tax Hardship Center for past due returns

Our services at Tax Hardship Center help you file old returns and reduce balances with practical options. Start with our Installment Agreement help if you need a monthly plan. If a settlement may fit, review our Offer in Compromise guidance. If money feels tight right now, our Currently Not Collectible status support can pause enforcement while you get current. For broader support, see our Services overview for full tax resolution and filings.

Protecting Social Security benefits and future refunds

Unpaid federal tax debt exposes a slice of your Social Security retirement benefits to a continuous federal levy. That levy can skim part of each check until you resolve the balance. Filing and setting a payment plan reduces that risk and may keep more cash in your pocket. Filing also preserves future refunds by keeping your account in good standing. Refunds can offset older balances, which shortens payoff time.

Practical safeguards

File old returns before benefits start if possible. If benefits already started, file and enter a payment plan to show compliance. Monitor your account online to watch offsets and levies. Keep copies of all correspondence.

Reducing stress by clearing unfiled returns

Back taxes make everyday tasks feel heavy. You fix that by finishing one year at a time. A clear checklist, a simple filing method, and steady weekly time blocks turn a pile into progress. Each filed year lowers your risk and raises your confidence. After two or three filings, momentum takes over and stress drops fast.

A simple rhythm that works

Pick one night a week. Gather forms, fill the return, mail or e-file, then log what you did. Repeat until you reach the current year. Celebrate small wins along the way to keep pace.

Catching up on taxes you missed

Life happens. Moves, job changes, health issues, and lost mail all play a part. The IRS expects you to file once you earn income over the filing threshold for that year. You bring yourself current by filing each missing year, oldest first, then paying or planning payments. If records look thin, use transcripts and employer copies to rebuild your files. When in doubt, involve a professional for accuracy and speed.

Order of attack

Start with the oldest year that still allows a refund. Then file remaining older years in sequence. Wrap with the most recent year to stop new penalties from starting.

What counts as back taxes and unfiled returns

Back taxes include unpaid balances from filed returns and taxes the IRS believes you owe for years you did not file. Unfiled returns include any required Form 1040 that never reached the IRS. The IRS tracks your income from W-2s, 1099s, and other forms, so unfiled years still sit on their radar. When you leave them unfiled, the IRS may build a return for you that ignores deductions and credits. Filing your own accurate return almost always helps you.

Documents that signal an unfiled year

W-2s, 1099-NEC, 1099-MISC, 1099-K, 1099-INT, 1099-DIV, 1099-B, and 1098-T. Notices that mention a missing return or a proposed assessment. Mortgage and loan applications asking for recent filed returns.

How many years back the IRS allows you to file

You can file as far back as you need for federal income taxes. The IRS accepts late returns for any prior year, but the benefits change by year. You generally have three years from the original due date to claim a refund. After that, your filing may still reduce an IRS estimate or clear your record, but you may not recover refunds. File anyway to cut balances and fix your file.

Filing window realities

Refunds expire after three years. Payment plans stay available even for older years. Old balances still accrue interest, so the longer you wait, the more you pay.

What happens if you leave old tax years unfiled

The IRS may file a substitute return that ignores your deductions and credits. That can create a higher balance and trigger collection. Liens can cloud your credit and property. Levies can hit wages or federal payments. Interest and penalties keep climbing until you resolve the debt.

The fix still works

You can replace a substitute return with your original return. You can ask for penalty relief after you file. You can set a payment plan that fits your budget. You can protect your assets by getting compliant.

How late can you file and still benefit?

You gain by filing even decades later. Filing stops the largest penalty and starts the process toward resolution. You still may qualify for payment plans, penalty relief, and a better tax figure than an IRS estimate. If the refund window remains open, you claim that money. If the window closed, you still lower debt and risk.

A quick rule of thumb

File now for every unfiled year. Claim refunds for years inside three years of the original due date. File older years to replace estimates and clear the path to a plan.

Deadlines for refunds on prior years

Refunds expire if you miss the claim window. That window usually ends three years after the original due date, including valid extensions. If your employer withheld taxes or you made estimated payments, you lose that refund if you file too late. File before the window closes to keep your cash.

Action steps

Check the calendar for each year. If a refund year sits near the three-year mark, prioritize that return. Mail it certified and track delivery.

When the IRS takes collection and enforcement actions and tax levy risks

If you receive letters, this guide to the IRS collection process explains common notices and what to do next.

Leaving years unfiled raises notice traffic and tax audit risk, especially when third-party forms report income the IRS already sees.

Once the IRS assesses a balance and sends notices, it can file liens and issue a tax levy. A levy can reach wages and certain federal payments, including part of Social Security retirement benefits. The IRS uses automated programs for many levies, so you want a filed return and a payment plan in place before that point. Compliance gives you leverage for relief.

How to stay ahead

File, enter a plan, and keep payments current. Open every IRS letter and respond on time. If a levy notice arrives, act the same day by contacting the IRS or a professional.

Filing late vs. not filing at all

Filing late beats not filing. Filing proves your actual tax and shuts down the steepest penalty. Not filing puts you at risk for a substitute return, levies, and bigger balances. Filing also puts you in line for payment options and penalty relief. Not filing removes your leverage and invites enforcement.

Bottom line

Send the return. Even if it will show a balance, filing starts a path to fix it.

How to file tax returns for previous years

Old returns follow the same core steps as current ones. You gather records, pick the correct year’s forms, prepare the return, and submit it by e-file or mail depending on the year. You keep proof, monitor processing, and plan any payments. You repeat the steps year by year until you reach current.

What to expect after filing

The IRS processes prior-year mailings more slowly than e-filed current-year returns. You may see offset refunds if you owe for other years. You receive letters if the IRS needs more information.

Gathering income records and tax forms for past years

Pull dividend forms like 1099-DIV in addition to interest, brokerage, and wage statements so your calculation lines match your return.

Start with the basics. Pull W-2s and all 1099s from clients, banks, brokers, and platforms. Add unemployment income forms, year-end rental income statements, and rental property expense summaries. Collect 1095-A forms if you used a marketplace health plan. Gather receipts and statements for deductions like mortgage interest, property taxes, charitable gifts to tax-exempt non-profits, and student loan interest. Use bank and card statements to rebuild records when originals went missing.

Where to find missing forms

Request copies from employers and payers. Download tax transcripts that list reported income. Check your email and payroll portals. For investments, pull year-end broker statements.

Downloading prior-year IRS tax forms

The IRS page on filing past due tax returns lists prior-year forms and instructions, plus VITA clinic options.

Use the correct form for the year you are filing. Prior-year Form 1040 and schedules match the rules and rates for that year. Using the wrong year’s form creates delays and notices. Download forms and instructions for each year you need, then fill them out completely and legibly.

Pro tip

Print instructions for each year and highlight special rules that apply to you, like education credits or self-employment deductions.

Using tax software for old returns

Most consumer tax software supports the current year and the two prior years for e-filing. Some providers also offer downloads for older years to help you prepare, but those returns still mail. Software speeds the math, checks common errors, and stores a running archive of what you filed. If your return includes a business, rentals, or multi-state income, choose software tiers that cover those schedules.

When software falls short

If you juggle multiple K-1s, complex capital gains, or basis tracking, move to a professional or a robust desktop product. Accuracy beats speed for these returns.

Filing paper returns when e-filing is not allowed

Once a tax year falls outside the e-file window, you must mail the return. Use the correct IRS address for your state and balance due. Sign every return in ink, include required schedules, and attach W-2s with withholding. Send each year in a separate envelope unless instructions say otherwise.

Mailing checklist

Hand-sign and date the return. Include payment vouchers if you pay by check. Use certified mail and keep the receipt. Add a copy of any IRS notice you aim to resolve.

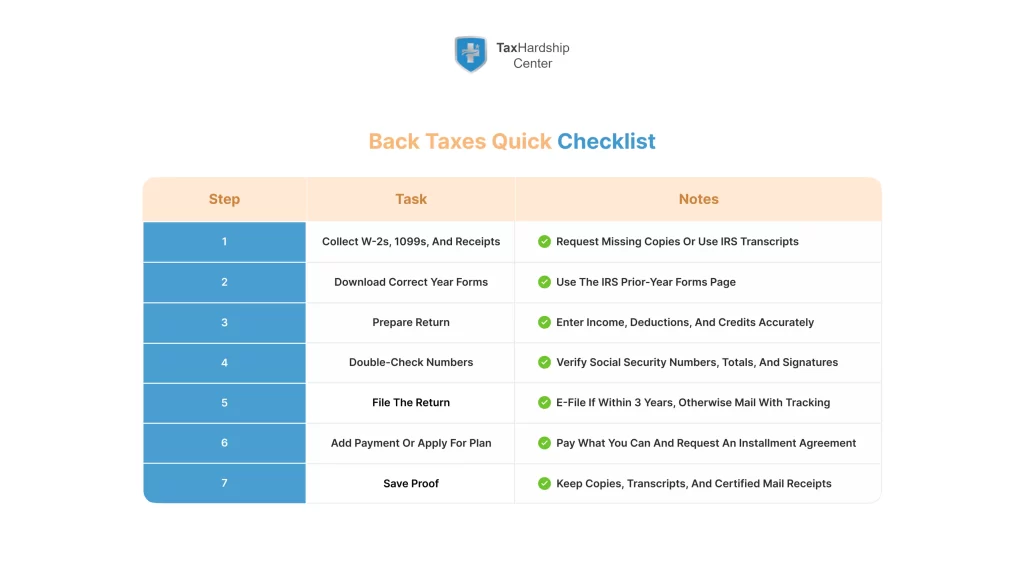

Step-by-step guide on how to file back taxes

You file old returns the same way every time, with a tight checklist and no shortcuts. Work year by year, oldest first, and keep your records clean. Use transcripts to fill gaps, pick the right forms, and capture every credit you deserve. Confirm delivery and track processing so nothing falls through the cracks. The steps below keep you moving without backtracking.

Step 1: Pull transcripts and income forms

Download wage and income transcripts. Request missing W-2s or 1099s from employers and payers. Build a folder for each year.

Step 2: Choose the correct year’s forms

Download the matching Form 1040 and schedules for that year. Read the instruction highlights for credits and deductions.

Step 3: Prepare the return

Enter income from W-2s, 1099s, and K-1s. Record deductions and credits. Review capital gains, basis, and wash sale rules for investment sales.

Step 4: Check the numbers

Run software checks or use printed worksheets. Confirm Social Security numbers, filing status, and bank routing for direct deposit.

Step 5: File the return

E-file if the year qualifies. Otherwise, mail with certified tracking. Attach W-2s and payment vouchers as needed.

Step 6: Set a payment plan if you owe

Apply online for a short-term or long-term installment agreement. Pick an amount you can sustain. Autopay if possible.

Step 7: Track the result

Watch your transcript for posting. Respond to any letter on time. Save copies of everything in your year folder.

Review IRS transcripts to confirm what was reported

Transcripts list income forms sent to the IRS under your name and Social Security number. They also show your adjusted gross income, payments, and account activity by year. Comparing your return to transcripts reduces missing income notices. Transcripts also confirm when the IRS posts your return and any payments. Keep a transcript in each year’s file as your official log.

Which transcripts to pull

Wage and Income Transcript for forms reported by third parties. Tax Return Transcript for key line items. Account Transcript for balances, penalties, and posting dates.

Calculate taxes owed including penalties and interest

You can estimate the total cost with a simple model. Start with the tax from your return. Add failure-to-file and failure-to-pay penalties, then layer interest to today’s date. Replace estimates with actuals once the IRS posts the return. If a payment plan starts, recalc with projected payments to map your payoff date.

Smart payment moves

Pay a lump sum with each filing to cut interest. Apply windfalls like bonuses or refunds from other years to the oldest balances. Revisit your plan if income drops or rises.

Send completed forms to the correct IRS address

Mailing to the right location speeds processing. IRS addresses vary by state and whether you include a payment. Use the address in the form instructions for the year you file. Put your Social Security number and tax year on the check if you mail a payment. Keep copies of everything you send.

Packaging tips

Use sturdy envelopes. Do not staple checks to returns. Place each year in its own envelope with its own certified mail slip and add a label with tags for the tax year and form.

Confirming receipt of your old tax return

Track certified mail delivery, then check your account transcript to confirm posting. If weeks pass without movement, call the IRS and reference your certified mail number. Keep that receipt with your copy of the return. Once posted, watch for notices that confirm the balance, offsets, or additional information requests.

What posting looks like

Your transcript shows a return received date and a posted date. It also shows subsequent payments and adjustments. Save a PDF copy.

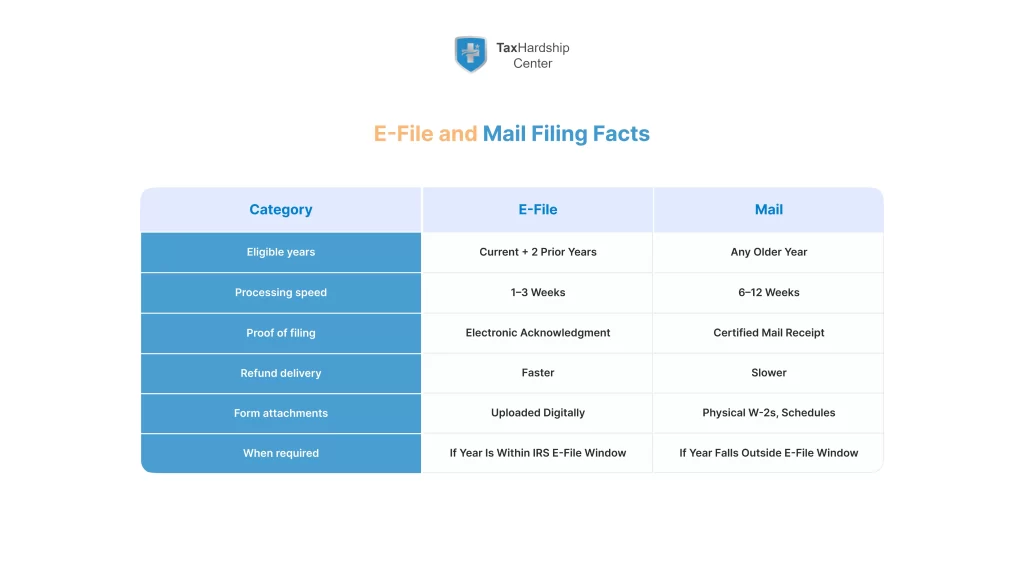

How to e-file prior-year tax returns

E-file speeds acceptance and reduces math errors. The IRS typically accepts the current year and the two prior years electronically through the modernized e-file system. If your software supports the year, e-file it. If it does not, print, sign, and mail.

What to check before e-filing

Confirm identity numbers, especially if you use an IP PIN. Verify direct deposit details. Use software diagnostics to catch errors before you hit submit. Run a quick readiness check inside your software before you press submit.

Which tax years allow electronic filing

Each January, the IRS opens e-file for the current year. The system also accepts the two prior years for a limited window. Returns older than that must go by mail. If you fall on the edge of that window, finish those years first to take advantage of e-file speed and error checks.

Why it matters

E-filed returns process faster, and you get confirmation quickly. Mail works, but it adds weeks to the timeline.

Using online tax software and tools

Online software guides you through income, deductions, and credits. It checks for common mistakes and keeps your documents in one place. For prior years still eligible for e-file, online platforms make the process faster. For older years, desktop software or fillable PDFs may fit better.

Pick the right tier

Choose a tax filing solution that supports self-employment, rental property, or investments if those apply. If you need multiple state returns, confirm the software supports them and state e-file. Review the provider website for transparent pricing, because some plans show strikethrough prices and prompt an upgrade during filing. Look for features that improve accuracy such as prior-year autofill, document upload, and desktop business returns for heavy schedules. Use a laptop when you handle many forms or multiple states. If you compare tools like taxact online, pick based on supported forms and help options, not ads.

When you must file prior-year returns by mail

Mail becomes your path when a year falls outside the e-file window, when a dependent ID mismatch blocks submission, or when a special attachment requires paper. Paper also fits when you amend multiple years at once and prefer a single package with a cover letter.

How to avoid delays

Type or print clearly. Include all schedules. Use tracked mail and keep copies.

What are the advantages of filing back taxes?

Filing opens doors that stay closed when you sit on old returns. You regain refunds for recent years. You get access to payment plans and settlement options. You improve your compliance history, which helps when you request penalty relief. You also stop substitute returns and cut down balances inflated by incomplete data.

Why lenders care

Mortgage underwriting standards usually require two years of filed returns, W-2s or 1099s, and bank statements.

Mortgage underwriters and business lenders often request the last two years of filed returns. Filing improves your odds for approval and better terms.

Claiming refunds you are owed

Check federal and state tax refund time frames so you know when funds should arrive and when to follow up.

If withholding or estimated payments exceeded your tax for a prior year, you may receive an income tax refund when you file within the statute. For businesses, a business tax refund can appear when payments or credits exceed liability for that year, or in years when carryback rules apply. Track your refund request and note the refund settlement date shown by your bank. Use direct deposit to a checking or savings account insured by the FDIC. Keep the confirmation email and save it in your Docs folder for that tax year.

Make refunds work for you

Direct deposit refunds into an account you set aside for tax payments. Apply refunds to the next year’s estimated taxes if your income rose.

Restoring eligibility for payment plans

The IRS expects you to file all required returns before it approves most payment plans. Filing clears that hurdle. Once approved, an installment agreement reduces active collection pressure and sets a steady monthly path to zero. Staying current on new filings keeps your plan in good standing.

What approval needs

Filed returns, a signed agreement, and a realistic monthly amount. Autopay helps you keep the plan active.

Rebuilding compliance history with the IRS

A clean streak of filed returns and on-time payments builds trust. That history helps when you request first-time abatement or argue reasonable cause for future hiccups. It also helps if you pursue a settlement option. Think of compliance as your credit score with the IRS.

Keep the streak alive

File early each season. Check your withholding or estimated payments to avoid new balances. Review transcripts once a quarter.

Options if you can’t pay your back taxes in full

You still file. Then you choose a path that fits your cash flow. Short-term plans give you up to 180 days to pay. Long-term plans spread the balance over many months. If payments would cause hardship, you can request a pause in collection. In rare cases, a settlement may apply.

Which path fits

If you can clear it in six months, use a short-term plan. If not, pick a long-term installment agreement. If bills outrun your income, consider a temporary hardship status.

IRS payment plans and installment agreements

You can also review the IRS page for payment plans and installment agreements and our explainer on the Streamlined Installment Agreement to compare options.

Run a quick calculation to choose a monthly dollar amount you can sustain and set a maximum you will not exceed.

An installment agreement sets a monthly payment that fits your budget. The IRS offers online applications for many balances, with setup fees that vary by payment method. Interest and a smaller penalty continue while you pay, but you keep control and avoid new levies. Make extra payments when you can to shorten the payoff.

Make the plan stick

Set autopay from a dedicated account. Review the plan each year after you file the new return. Increase payments when income improves.

Requesting penalty abatement or hardship relief

You may qualify for first-time abatement if you filed and paid on time for the prior three years and meet other rules. You may also receive relief if you show reasonable cause, such as serious illness or natural disaster, with documentation. If payments would leave you unable to meet basic needs, ask for temporary hardship status that pauses active collection.

How to ask well

File first, then request relief in writing or by phone. Keep dates, names, and copies of proof. Stay polite and specific.

Offers in compromise as a last resort

If you want a step-by-step view, our blog on IRS Form 656 for an Offer in Compromise shows forms, fees, and timelines.

An offer in compromise lets you settle for less than the full amount when you cannot pay in full and your financials prove it. Most offers require complete disclosure of assets, income, and expenses. Many do not qualify, so you prepare carefully and file only when your numbers support acceptance. Always stay current on new filings and payments during the process.

When an offer makes sense

You have limited equity, modest income, and little free cash after necessary expenses. Other plans would take longer than the collection statute that remains.

When to seek help from a tax professional

Ask about availability during filing season, response times, and whether phone or chat support fits your schedule.

Bring in a pro when returns span many years, include business income, or involve audits and levies. A licensed pro brings expertise on transcripts, statutes, and settlement options. You save time and reduce risk of errors that trigger notices. A pro also brings calm to tense calls with the IRS.

Who to hire

Look for an enrolled agent, CPA, or tax attorney with back-tax experience. Ask about years handled, acceptance rates for plans, and average timelines.

Complex returns with multiple income sources

Multiple jobs, self-employment, rentals, investments, and side gigs complicate old returns. You must track basis, depreciation, and business deductions across years. Software may not handle every case cleanly. A pro streamlines the data and helps you avoid double counting or missed carryovers.

Common pitfalls

Missing 1099-K income from platforms. Incorrect basis on stock sales. Skipping self-employment tax or the qualified business income deduction where allowed.

Back taxes with capital gains or business income and the Schedule C tax form

Markets and businesses change year to year. For sole proprietors, the Schedule C tax form needs clean books, consistent proprietor data, and clear categories for income and expenses. Your returns must follow the rules for each specific year, including capital gains rates and Section 179 limits. If you sold a home, review exclusion rules. If you ran losses, confirm carrybacks or carryforwards under that year’s law. Accuracy on these lines saves real money and prevents amended returns later.

Records to assemble

Broker statements with basis, K-1s, fixed asset lists, mileage logs, and home office records if they apply.

How a tax professional can communicate with the IRS for you

With a signed power of attorney, a pro can call the IRS, request transcripts, and negotiate plans on your behalf. That removes hours on hold and tough conversations from your plate. Pros also know which department to call and how to document agreements. You focus on your work while the process moves forward.

What you still handle

You collect documents, sign returns, and approve plans. You stay current on new filings and payments while the pro handles the back work.

Tax tips and tools for staying current in future years

Staying current beats catching up. You set calendar reminders, keep a digital tax folder, and download transcripts each summer to check your file. You adjust withholding after raises and side income. You keep receipts as you go instead of scrambling in April. Small habits make filing easy year after year.

A simple setup

Create a cloud folder named Taxes with subfolders by year. Drop W-2s, 1099s, and big receipts in as they arrive. Keep a one-page checklist in each folder.

Using IRS online tax tools and transcripts on the IRS website

If you qualify for the IRS Volunteer Income Tax Assistance program, often called VITA, local sites across the United States can help you file with accuracy at no cost.

An IRS Online Account on the IRS website gives you access to transcripts, balances, and payment history with stronger accuracy. You can view prior AGI for e-file PINs, confirm offsets, and print records for lenders. You also receive secure messages and alerts. Download PDFs of key docs and tag each file by year in your cloud folder so retrieval takes seconds. Checking your account a few times a year prevents surprises and keeps you informed.

What to review quarterly

Account balances, pending payments, transcript updates, and any new income forms reported under your Social Security number.

Setting reminders for annual tax filing deadlines

Put key dates on your calendar for filing and estimated payments. Add a prep day two weeks before each deadline to gather documents. Set alerts at 30, 7, and 1 day out. A simple schedule removes last-minute stress and late fees.

Dates to mark

January wage and income forms arrive. April filing deadline for most taxpayers. June and September estimated payment dates if you owe quarterly. October extension deadline if you filed an extension.

Choosing simple tax preparation methods for on-time filing and accuracy

Start by judging your tax complexity and read each provider’s disclaimer before you commit. Some products market an audit support guarantee or a max refund claim in advertisements; review limits carefully.

Match your method to your situation and aim for accuracy over speed. If your return stays simple, online software offers a guided path. If your return includes a business, a subsidiary, non-profits reporting, or complex investments, use a pro or robust desktop software. Read the provider website disclosures and consent preferences before you start. Simpler methods lead to fewer errors and faster filings.

A quick decision tree

W-2 only and standard deduction: online software. Self-employment or rentals: desktop software or a pro. Multi-state, K-1s, or complex gains: hire a pro.

How Tax Hardship Center can help with past due returns

At Tax Hardship Center, we help you file old returns and resolve balances with the right tool for your case. Explore our Installment Agreement help, Offer in Compromise guidance, and Currently Not Collectible support. For bookkeeping and ongoing filings, see our Services overview.

You want a clear plan, accurate filings, and steady progress. Our team at Tax Hardship Center prepares prior-year returns, organizes transcripts, and builds a filing sequence that protects refund claims. We file fast, document every step, and explain each decision in plain language. We guide you through payment options and penalty relief so you regain control without guesswork.

Professional IRS back tax filing help

We prepare returns from simple W-2 years to complex Schedules C, E, and D. We rebuild records when forms went missing. We verify every number against transcripts to avoid notices. We package mailings for older years and confirm delivery, posting, and next steps.

Negotiating payment solutions and reducing penalties

We set up installment agreements that fit real budgets. We request first-time abatement where you qualify and build strong reasonable cause cases when life events justify relief. When facts support it, we evaluate offers in compromise and manage the process end to end while you stay current on new filings.

In summary…

A clear, steady process solves old taxes. You file each missing year, confirm posting, and set payments that fit your budget. You protect refunds inside the statute and cut penalties by filing now. You track progress with transcripts and keep your new filings on time so the problem stays solved.

- File first to stop the largest penalty.

- Use the correct year’s forms and e-file when allowed.

- Mail older years with certified tracking.

- Use the correct year’s forms and e-file when allowed.

- Protect cash and benefits.

- Claim refunds within three years of the due date.

- Set a payment plan to reduce levy risk and interest.

- Claim refunds within three years of the due date.

- Use tools that keep you current.

- Pull transcripts, set calendar reminders, and adjust withholding.

- Keep documents in a yearly digital folder.

- Pull transcripts, set calendar reminders, and adjust withholding.

- Get help when returns turn complex.

- Hire a licensed pro for multi-year, multi-source income.

- Let a pro speak with the IRS so you can stay focused on work.

- Hire a licensed pro for multi-year, multi-source income.

Filing fixes the past and frees your future cash flow. If you want a straight path from unfiled to compliant, reach out to Tax Hardship Center. We will map the years, handle the filings, and set the plan so you can get back to life.

FAQs

Can I file taxes from 10 years ago?

Yes. You can file any prior year. You may not receive a refund for very old years because the refund window usually closes three years after the original due date. File anyway to reduce balances and fix your records.

How far back will the IRS accept e-filed returns?

Typically the IRS accepts the current year and the two prior years electronically. Older years must go by mail. If you sit on the edge of that window, finish those years first to use e-file.

What if I can’t find my W-2 or 1099 forms?

Request copies from your employer or payer and pull wage and income transcripts. Those transcripts list what third parties reported under your Social Security number, which helps you complete the return accurately.

Will filing old returns trigger an audit?

Filing itself does not target you for an audit. Inaccurate or incomplete returns raise risk. Using transcripts, correct forms, and clear records lowers notice risk.

Should I file if I can’t pay the full amount?

Yes. Filing cuts the biggest penalty and opens the door to payment plans, penalty relief, and other options. Pay what you can with the return and set a plan for the rest.