Introduction

Tax relief sits at the center of many decisions that determine how U.S. taxpayers manage financial pressure, unexpected obligations, and long-term planning. The term refers to a collection of mechanisms designed to reduce the burden of taxes or make paying them more manageable. While many people associate tax relief only with IRS debt settlement programs, the concept extends across credits, deductions, hardship arrangements, disaster provisions, and structured negotiations with the Internal Revenue Service. Each category interacts with specific conditions such as income, family status, assets, residency, and past compliance behavior.

When tax bills exceed a manageable threshold, the federal and state tax systems offer structured pathways to limit financial strain. These pathways operate through different entities, each with its own attributes and rules. Tax credits directly reduce the amount owed; deductions reduce taxable income; tax debt relief programs restructure or reduce unpaid liabilities; hardship-based relief pauses collection activity; and disaster-related adjustments protect taxpayers facing extraordinary circumstances.

Understanding these mechanisms is essential because relief is not applied automatically. It must be claimed, requested, negotiated, or qualified for based on documented facts. Missing the opportunity to apply for relief can lead to larger balances due to penalties, interest, and enforced collection. Knowing the options available gives taxpayers the clarity needed to identify the correct route early, gather the necessary documentation, and determine when professional representation is required.

Key Takeaways

• Tax relief refers to structured methods that reduce tax liability, restructure debt, or ease payment obligations.

• Relief can take the form of credits, deductions, hardship status, disaster adjustments, or IRS negotiation programs.

• Eligibility varies according to income, assets, prior filings, financial hardship, and state-level differences.

• Failure to seek relief promptly often results in penalties, interest accrual, and enforced IRS collection.

• Understanding relief categories prepares taxpayers to identify the appropriate program and documentation required.

Understanding the Concept of Tax Relief

The concept of tax relief functions as an umbrella for several distinct mechanisms within federal and state tax systems. Each mechanism addresses a different taxpayer need, yet all share a common purpose: reducing the impact of taxes or making payment obligations more feasible. Relief is built around statutory authority, administrative discretion, and documented taxpayer circumstances.

Tax relief can be categorized across several entities: tax credits, tax deductions, exclusions, debt-relief programs, penalty adjustments, and temporary relief measures. Each entity has specific attributes that determine how it affects liability. Credits reduce the final amount owed. Deductions reduce taxable income. Exclusions exempt certain income from taxation. Debt-relief programs restructure or reduce unpaid liabilities based on the ability to pay. Penalty abatements remove or reduce charges that accumulate when tax obligations are not met in time. Temporary relief applies during disasters, major disruptions, or recognized hardships.

These forms of relief attach to predicates such as qualifying, applying, claiming, negotiating, verifying, and documenting. Their use depends on interactions between taxpayer income, compliance records, household composition, dependents, wages, self-employment activity, allowable expenses, and assets. Relief pathways vary widely depending on whether a taxpayer is current with filings, falls within low-income thresholds, has suffered a qualifying hardship, or faces an IRS balance that cannot be fully paid.

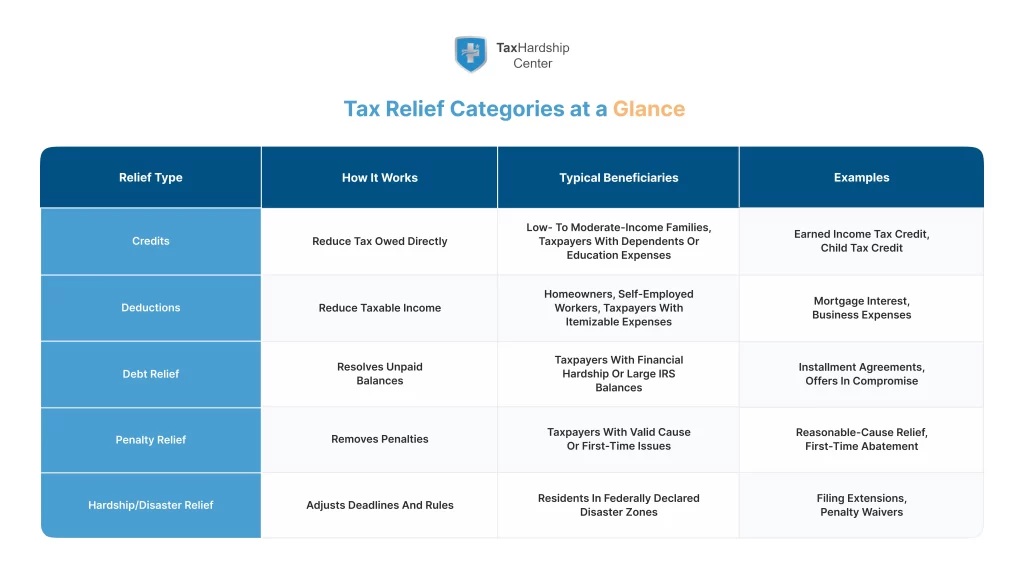

A table helps clarify the distinctions:

| Relief Type | Core Function | Typical Trigger | Interaction With IRS or State |

| Tax credit | Reduces tax owed | Dependents, education, and earned income | Claimed on return |

| Tax deduction | Reduces taxable income | Mortgage interest, business expenses | Claimed on return |

| Debt relief program | Reduces or restructures debt | Inability to pay | Requires application and documentation |

| Penalty adjustment | Removes penalties | Reasonable cause, timely response | IRS review required |

| Temporary relief | Adjusts deadlines or rules | Disaster or emergency | IRS or state announcement |

These components show that tax relief is not a single action but a detailed network of interconnected entities, each functioning under specific conditions.

Why Tax Relief Matters for U.S. Taxpayers

Tax relief plays a significant role in helping individuals and households maintain financial stability when obligations rise beyond their immediate capacity. Many taxpayers experience periods when income drops, unexpected expenses arise, or past filings result in unresolved balances. In these situations, tax relief mechanisms act as structured protections that prevent manageable issues from escalating into long-term financial strain.

IRS collection activity is an essential entity within this system. Once a balance becomes overdue, the IRS initiates a sequence that can include notices, interest accrual, penalties, liens, and wage garnishment. Tax relief programs interact directly with these enforcement steps through predicates such as pausing, reducing, or restructuring the liability. For instance, a hardship determination can temporarily halt levies, while an installment agreement restructures repayment into predictable monthly amounts.

Relief also matters for taxpayers who remain current on filings but experience shifting eligibility for credits or deductions. Household changes, employment transitions, state-specific provisions, and dependents create new opportunities for relief each year. Tax credits tied to income levels, childcare, and earned income provide meaningful support when claimed correctly. When left unclaimed, they create missed financial benefits that could reduce financial strain or offset past debt.

Disaster relief is another significant dimension. Federal and state authorities modify deadlines, waive penalties, or adjust rules when severe events affect entire regions. Families facing natural disasters often rely on these provisions to regain financial footing.

The importance of tax relief becomes clearer when looking at repeat interactions. A taxpayer who files late, ignores notices, or assumes tax debt cannot be negotiated may encounter escalating consequences. Structured relief options counter these risks by offering controlled pathways that reflect actual financial conditions. These pathways align the IRS’s authority to collect with the taxpayer’s documented ability to pay.

Tax relief matters because it transforms rigid obligations into manageable arrangements. It reduces unmanageable burdens, supports families facing hardship, and creates a process for resolving tax debt without unnecessary escalation.

Types of Tax Relief for U.S. Taxpayers

Tax relief appears in multiple forms, each reflecting different relationships between taxpayer circumstances, statutory rules, and administrative procedures. These forms vary in how they reduce liability, the documentation required, and how federal or state authorities evaluate eligibility. Understanding these distinctions makes it easier to identify which option aligns with a particular financial situation.

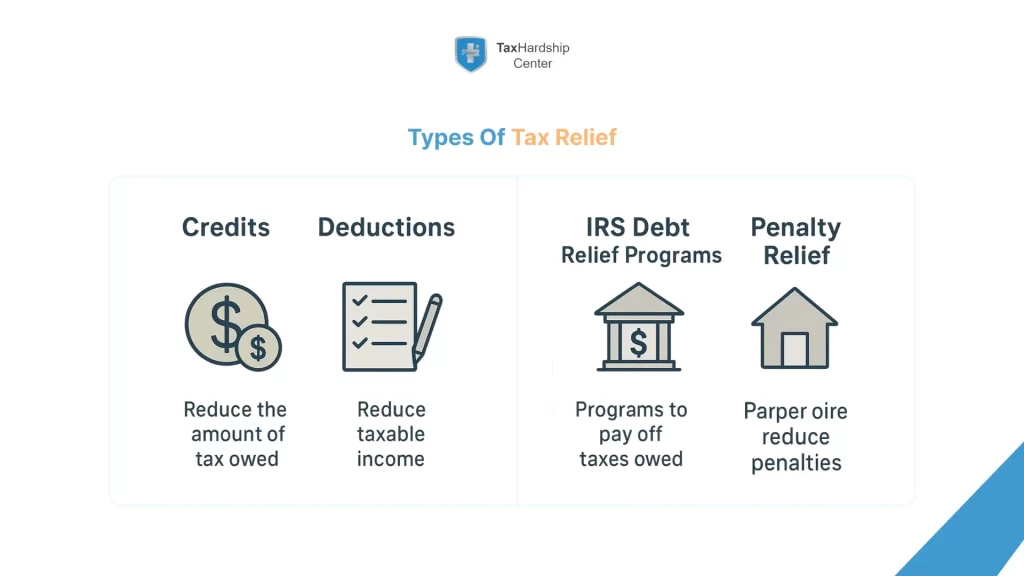

Tax credits function as direct reductions in the amount owed. Credits attach to predicates such as claiming dependents, reporting earned income, paying qualified education expenses, or meeting low-income thresholds. Refundable credits can generate a refund even when no tax is owed, while non-refundable credits reduce liability only to zero.

Tax deductions and exclusions operate on the income side of the equation. Deductions reduce taxable income by allowing qualified expenses for mortgage interest, business costs, medical expenses, or retirement contributions. Exclusions remove certain types of income from taxation, including some employer benefits and specific disaster-related payments.

Debt-related relief applies when taxpayers owe the IRS or state authorities and cannot pay in full. Several programs are built around ability-to-pay assessments. An Offer in Compromise (OIC) assistance evaluates equity in assets, income patterns, necessary expenses, and future earning potential to determine if a reduced settlement is appropriate. Installment agreements restructure the debt into scheduled payments. Currently Not Collectible status pauses collection when documented hardship prevents any payment.

Penalty adjustments address charges that accumulate when deadlines are missed or information is inaccurate. Abatements depend on predicates such as reasonable cause, medical emergencies, natural disasters, or documented obstacles that made compliance impractical.

Temporary relief appears when emergencies or disasters disrupt a region. Measures include deadline extensions, waivers of specific penalties, and adjustments tied to federally declared events.

A structural comparison clarifies the categories:

| Category | Core Effect | Evidence Generally Required |

| Credits | Direct reduction of tax owed | Eligibility documents (income, dependents, expenses) |

| Deductions | Lower taxable income | Expense records, business logs, interest statements |

| Debt relief | Reduced or restructured liability | Financial statements, hardship evidence |

| Penalty relief | Removal of added charges | Reasonable-cause documentation |

| Temporary relief | Deadline and rule adjustments | Residence or business location in affected area |

These categories represent the primary avenues through which taxpayers reduce tax pressure or resolve existing obligations.

How to Qualify for Tax Relief Programs

Qualifying for tax relief depends on the interaction between the taxpayer’s financial conditions, compliance history, legal requirements, and the evidence presented to federal or state authorities. Each relief category operates under distinct criteria, yet they all rely on documented facts that show eligibility.

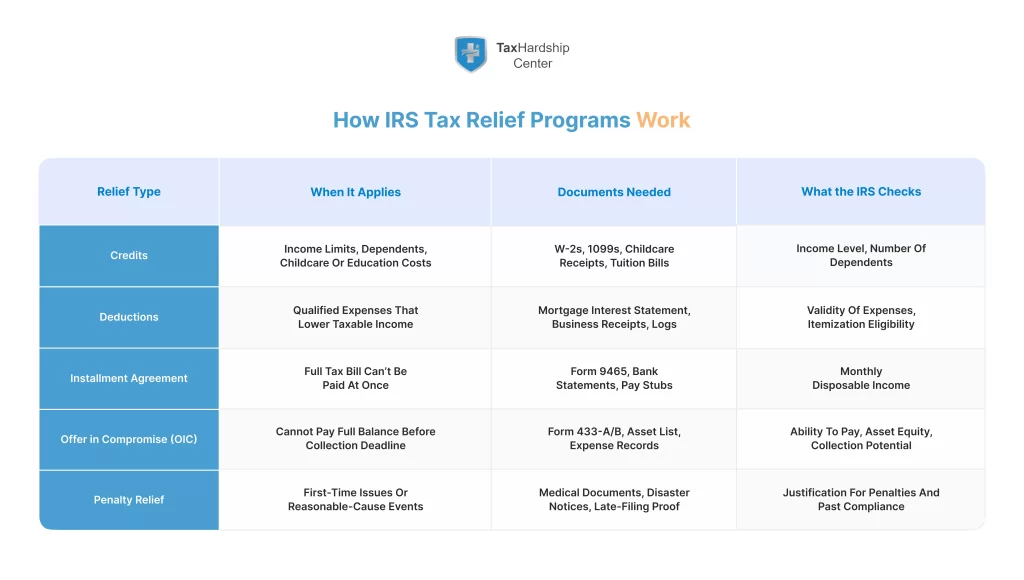

Qualifying for a tax credit requires records that confirm income limits, dependent status, childcare costs, tuition payments, or other criteria defined by the statute. Income thresholds determine whether a credit remains available, phases out, or becomes refundable. Accurate filings and supporting documents allow federal and state systems to apply the credit correctly.

Qualifying for deductions and exclusions requires documentation showing that expenses or income fall within the tax code definitions. For example, mortgage interest deductions rely on lender statements, while business deductions rely on organized expense tracking and evidence of ordinary and necessary costs.

Debt-focused programs use a more extensive evaluation process. The IRS examines the taxpayer’s ability to pay through financial disclosures that outline income, assets, equity, necessary living expenses, and liabilities. This process often includes Form 433-A or 433-F, both of which detail wage data, bank accounts, real estate equity, vehicles, and monthly obligations. Eligibility hinges on demonstrating that full payment would create financial hardship or exceed reasonable collection potential.

Penalty abatement uses a different standard. Reasonable-cause explanations must show circumstances that prevented timely filing or payment. Documentation may involve medical records, natural-disaster notices, or other verifiable events.

A typical qualification sequence follows these steps:

- Identifying the applicable relief category based on the type of tax issue.

- Gathering supporting records such as income statements, expense logs, bank reports, and prior tax filings.

- Completing the correct forms for the relief category.

- Submitting documentation to tax authorities or representatives.

- Responding to additional information requests if required.

State-level criteria may differ from federal rules. Some states require separate filings for credits or disaster relief, while others rely on the federal return for verification. Multi-state earners may need to establish residency periods or allocate income across jurisdictions before relief is granted.

Qualification depends on accurate documentation and a clear demonstration of financial or statutory eligibility, making thorough preparation essential before applying.

Working With a Tax Relief Service

Tax relief services represent taxpayers before federal and state authorities and manage the procedural steps required to secure specific forms of relief. These services rely on trained professionals who interpret tax rules, prepare documentation, and address compliance issues that shape eligibility outcomes.

A tax relief service typically evaluates the taxpayer’s financial condition through a structured review of income patterns, expense categories, and asset holdings. This assessment establishes which relief pathways may be viable. Once viable routes are identified, representatives prepare the required forms, coordinate filings, and interact directly with the IRS or state agencies. This interaction includes submitting financial disclosures, negotiating installment terms, presenting hardship evidence, or requesting penalty adjustments.

Services are particularly valuable when tax debt exceeds the taxpayer’s capacity to pay, when enforcement actions have begun, or when documentation requirements are extensive. For example, negotiating an Offer in Compromise requires detailed analysis of equity and income, as well as strict adherence to IRS formula calculations. A service can navigate these calculations and present a structured case that reflects the taxpayer’s actual ability to pay.

Evaluating a tax relief service involves examining several attributes: representatives’ credentials, transparency in fees, clarity about service scope, communication patterns, and documented case experience. A reputable service provides clear expectations without guaranteeing unrealistic outcomes. Fee structures may include initial assessment charges, flat rates for specific services, or phased billing tied to case progress.

A typical service workflow follows this pattern:

- Preliminary financial review and identification of potential relief options.

- Collection and organization of tax records, bank statements, pay information, and expense details.

- Preparation of IRS or state forms based on the relief category.

- Submission of documentation and communication with tax authorities.

- Negotiation or advocacy based on the taxpayer’s financial profile.

- Monitoring follow-up requests or additional document requirements.

Tax relief services also assist individuals with multi-state obligations, business tax issues, or long-standing unfiled returns. Their role becomes crucial when a taxpayer faces liens, wage garnishment, or escalating penalties that require immediate action.

State vs Federal Tax Relief – What to Know

Federal and state tax relief systems operate under separate authorities, each using its own statutes, definitions, and procedural rules. Although they may share terminology, their programs often differ in scope, eligibility, and required documentation. Understanding these differences helps prevent incorrect filings, delays, or incomplete claims.

The IRS administers federal tax relief. Its programs focus on nationwide tax rules that apply uniformly across all states. These programs include tax credits, deductions, penalty abatements, hardship determinations, installment agreements, and settlement procedures. The IRS evaluates federal relief requests based on income, dependents, filing status, assets, and the taxpayer’s ability to pay. When tax debt exists, federal relief programs rely on standardized calculations to measure necessary living expenses, disposable income, and asset equity to determine eligibility.

State-level relief varies widely. Each state sets its own credit structures, tax brackets, earned income thresholds, disaster declarations, and enforcement practices. Relief may include state-specific refundable credits, property tax adjustments, disaster-related filing extensions, and state-level debt-repayment agreements. Some states operate independent debt settlement programs similar to federal offerings, while others limit relief to payment plans or hardship-based enforcement pauses.

A simple comparison shows the structural contrast:

| Category | Federal Relief | State Relief |

| Governing authority | IRS | State tax department |

| Eligibility rules | Uniform nationwide | Vary by state |

| Credit structures | Extensive and standardized | Often narrower or state-specific |

| Debt relief programs | Offers, payment plans, hardship status | Depends on state; may be limited |

| Disaster measures | Declared by federal agencies | Declared by state governors or local authorities |

| Documentation | Federal forms, standard disclosures | Depends on the state; may be limited |

Where taxpayers owe both federal and state taxes, each authority manages its own collection process. Federal liens and state liens can run concurrently. Payment plans may need to be negotiated separately. In multi-state cases, such as when workers move during the year, eligibility for state relief may depend on residency periods or income allocation rules. Coordinating relief across jurisdictions requires accurate recordkeeping and a clear understanding of how federal and state regulations interact.

State and federal relief systems work in parallel rather than in sequence. Recognizing this separation prevents misunderstandings and ensures that relief opportunities are not overlooked on either level.

Common Mistakes and How to Avoid Them

Many taxpayers miss available relief or encounter avoidable complications because of preventable errors in filing, documentation, or decision-making. These mistakes often arise from misunderstandings about eligibility, assumptions about IRS procedures, or delays in responding to notices.

One of the most common mistakes involves overlooking available credits or deductions. Taxpayers may assume they do not qualify, fail to claim credits tied to dependents or income levels, or misinterpret state-level eligibility. Missing these opportunities increases liability and reduces access to future relief options.

Another widespread issue occurs when individuals attempt to resolve tax debt without understanding how the IRS evaluates their ability to pay. Submitting incomplete financial disclosures, understating assets, or failing to document essential expenses creates inconsistencies that lead to denials. Relief programs require transparent records, including bank statements, pay information, loan details, and any assets that may affect settlement calculations.

Engaging unqualified or misleading tax relief firms creates additional risk. Some firms promise unrealistic outcomes or fail to communicate accurately with tax authorities. Choosing a provider without reviewing credentials, service scope, or fee structure can lead to wasted time and unresolved liabilities.

Ignoring state obligations is another frequent error. Many taxpayers focus exclusively on federal filings and overlook state debts, leading to parallel penalties or state-level enforcement actions. Each authority operates independently, so resolving federal issues does not address state requirements.

Delaying action often leads to higher penalties, interest accumulation, and expanded enforcement. IRS notices escalate through predictable stages. Waiting until garnishments or liens occur reduces available negotiation options and increases documentation demands.

A list of common pitfalls includes:

- Missing eligibility for credits or deductions

- Submitting incomplete relief applications

- Underestimating documentation requirements

- Overlooking state tax obligations

- Choosing firms without verifying their credentials

- Waiting until enforcement actions begin

Avoiding these mistakes requires timely filing, accurate recordkeeping, understanding available relief pathways, and selecting qualified assistance when needed.

How to Choose the Right Tax Relief Partner

Selecting a tax relief partner requires careful evaluation of expertise, procedural knowledge, and the ability to manage communication with tax authorities. Because tax relief depends on accurate financial disclosures and organized filings, the quality of representation directly affects the outcome of settlement negotiations, penalty reviews, and debt-related resolutions.

The most reliable partners employ professionals authorized to represent taxpayers before the IRS, such as enrolled agents, certified public accountants, or tax attorneys. These credentials indicate familiarity with IRS collection standards, financial analysis requirements, and the structure of federal and state relief programs. Firms like Tax Hardship Center employ credentialed specialists who work with financial statements, IRS forms, and settlement procedures daily, thereby strengthening the accuracy of case preparation.

Transparent service models are another key factor. A dependable partner explains costs, outlines service stages, and provides realistic expectations based on documented financial conditions rather than speculative outcomes. Legitimate firms avoid guarantees regarding programs such as Offers in Compromise or penalty abatements, since the IRS determines approval after reviewing submitted financial disclosures.

Service scope should also be examined. Some firms focus narrowly on federal debt relief, while others, including Tax Hardship Center, assist with unfiled returns, state-level negotiations, penalty reduction requests, and multi-year compliance corrections. Broader coverage helps when tax issues overlap across jurisdictions or when multiple years require amendment.

Clear communication plays a vital role in maintaining progress. A capable firm provides updates, requests documents in an organized manner, and responds promptly to new IRS inquiries. This reduces delays and ensures that supporting evidence aligns with IRS evaluation processes.

Helpful evaluation points include:

- Verification of representative credentials

- Review of documented service scope

- Transparency in fee structures

- Expected timelines for each relief category

- Communication reliability and documentation standards

- Experience with similar case types

Selecting a qualified partner improves the accuracy and completeness of relief applications. Firms with structured processes, such as Tax Hardship Center, provide disciplined representation that aligns financial documentation with relief pathways recognized by federal and state authorities.

Conclusion

Tax relief represents a structured set of methods that reduce tax burdens, reorganize payments, or address hardships that interfere with timely compliance. These methods span across credits, deductions, penalty reductions, settlement programs, installment arrangements, and disaster-related adjustments. Each type of relief interacts with specific financial conditions, asset structures, and documentation requirements.

The importance of relief becomes clear when tax obligations escalate. Penalties, interest, and enforcement actions escalate rapidly when filings fall behind or balances remain unpaid. Relief programs provide structured pathways that match obligations with financial capacity. They also help prevent unnecessary escalation, reduce financial pressure, and restore compliance for individuals and businesses.

The successful use of relief programs depends on accurate documentation, understanding of eligibility requirements, and timely engagement with federal and state authorities. Financial disclosures, income verification, asset valuations, expense summaries, and complete filing histories form the foundation of all relief decisions.

Professional representation can assist when circumstances are complex or when settlement negotiations require detailed financial analysis. Firms such as Tax Hardship Center support taxpayers by preparing disclosures, coordinating filings, evaluating available relief, and communicating with tax authorities. This structured support is especially important in cases involving large balances, multi-year noncompliance, or state and federal overlaps.

Tax relief provides an organized way to address liabilities in accordance with statutory rules and documented financial realities. By identifying the appropriate form of relief and presenting accurate evidence, taxpayers can discharge their obligations while maintaining financial stability.

FAQ’s:

What qualifies as tax relief from the IRS?

Tax relief from the IRS includes any approved method that reduces liability, restructures debt, removes penalties, or delays collection due to hardship. Eligibility depends on documented financial conditions, compliance history, and statutory requirements. Services such as Tax Hardship Center evaluate these factors through financial reviews that identify which federal programs may apply.

How does an Offer in Compromise work?

An Offer in Compromise allows settlement of federal tax debt for less than the full amount when financial disclosures show limited ability to pay. The IRS reviews income patterns, assets, equity, and necessary living expenses to determine reasonable collection potential. Relief firms familiar with IRS formulas, including the Tax Hardship Center, organize financial statements and prepare submissions that align with IRS evaluation standards.

Can tax relief apply to past unfiled returns?

Relief programs can be applied for once all required returns have been filed. Unfiled returns prevent debt restructuring, penalty reviews, or settlement negotiations from moving forward. Assistance from a relief service can help prepare multiple-year filings and assemble the supporting documentation needed to bring accounts into compliance.

Does state tax relief function the same way as federal tax relief?

State tax relief operates independently and may follow different eligibility rules, credit structures, and hardship standards. Some states offer payment plans, disaster extensions, or limited penalty reductions. Firms such as Tax Hardship Center often handle both state and federal cases, enabling coordinated guidance when obligations span jurisdictions.

How long does the IRS consider tax debt collectible?

The IRS typically maintains the ability to collect federal tax debt for ten years from the date the liability is assessed. This period is known as the collection statute expiration date. Relief programs, payment plans, and financial reviews often consider how much time remains before the statute expires. Structured representation ensures that disclosures and filings account for the remaining collection window.

Can penalty relief be requested more than once?

Penalty relief may be available multiple times when supported by reasonable-cause evidence. However, the first-time penalty abatement applies only once per compliance period. Documented hardship, natural disasters, or medical events may support additional relief requests. Relief firms frequently assist with compiling evidence in a format recognized by tax authorities.

Will enrolling in a tax relief program affect credit?

IRS tax debt and relief enrollment do not appear directly on credit reports. However, a federal tax lien filed in the public record may be visible to lenders during certain checks. Relief programs help reduce the likelihood of lien escalation by placing accounts into structured arrangements such as installment agreements or hardship status.